1. Off‑Highway Vehicle Telematics Market Overview - Definition, scope, and significance?

Off‑highway vehicle (OHV) telematics refers to the integration of hardware, software and communication technologies that collect, transmit and analyze data from equipment such as excavators, tractors, haul trucks and loaders operating outside conventional road networks. The scope covers connectivity solutions (cellular‑based, satellite‑based), data‑analytics platforms and service models that enable real‑time vehicle monitoring, predictive maintenance, fuel optimization and operator safety across construction, agriculture and mining sectors. Its significance lies in improving asset utilization, reducing downtime, enhancing safety compliance and delivering measurable cost savings for capital‑intensive fleets.

2. Off‑Highway Vehicle Telematics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for fleet efficiency, stringent emissions regulations, and the digital transformation of heavy‑equipment manufacturers. The ability to remotely monitor equipment in remote sites drives adoption especially in mining and large‑scale construction projects. Restraints stem from high upfront installation costs, limited broadband coverage in isolated locations, and data‑security concerns. Challenges involve integrating heterogeneous sensor standards and ensuring interoperability across legacy equipment. Opportunities arise from emerging low‑power wide‑area networks (LPWAN) such as LTE‑M and NB‑IoT, the expansion of satellite constellations for ubiquitous coverage, and the growing appetite for value‑added services like usage‑based insurance and autonomous‑vehicle support.

3. Off‑Highway Vehicle Telematics Market Growth Trends - Current and emerging trends shaping the market?

The market is witnessing a shift from proprietary radio links to standardized IoT protocols, with LTE‑M and NB‑IoT gaining traction for their low latency and power efficiency. Satellite‑based telematics is expanding beyond oil & gas into construction and mining where cellular coverage is sparse. Data‑analytics is moving from descriptive dashboards to predictive AI models that forecast component failure and optimize route planning. Additionally, OEMs are bundling telematics with equipment sales, creating subscription‑based revenue streams, while third‑party platforms are offering open APIs to foster ecosystem development.

4. COVID‑19 Impact on the Off‑Highway Vehicle Telematics Market - Pandemic effects and recovery trajectory?

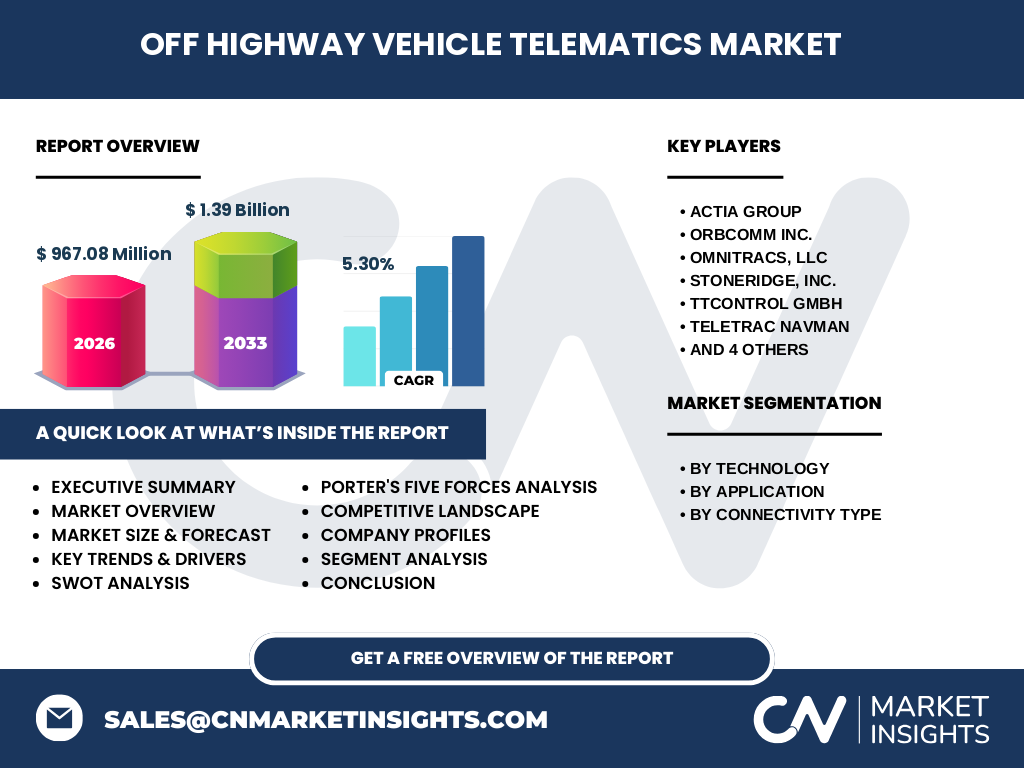

During the peak of the pandemic, project delays and reduced capital expenditure temporarily slowed new telematics deployments. However, the need for remote monitoring and reduced on‑site personnel heightened the perceived value of telematics solutions. As construction, agriculture and mining activities resumed, the market entered a rapid recovery phase, with firms accelerating digital initiatives to recoup lost productivity. This post‑COVID momentum is reflected in the projected growth from a 2026 market size of USD 967.08 million to an estimated USD 1.39 billion by 2033.

5. Off‑Highway Vehicle Telematics Market Competitive Landscape - Major competitors and market consolidation?

The competitive arena consists of specialist telematics providers and equipment manufacturers that have developed in‑house platforms. Notable players include ACTIA Group, ORBCOMM Inc., Omnitracs, LLC, Stoneridge, Inc., TTControl GmbH, Teletrac Navman, TomTom Telematics BV, Trackunit A/S, Wacker Neuson SE and Zonar Systems Inc. Recent years have seen strategic alliances and selective acquisitions aimed at expanding geographic reach and technology portfolios, but the market remains fragmented with no single entity commanding a dominant share.

6. Executive Summary - High‑level overview and key findings about Off‑Highway Vehicle Telematics Market?

The Off‑Highway Vehicle Telematics market is positioned for robust growth, driven by efficiency demands and the rollout of LPWAN and satellite connectivity. With a 2026 valuation of USD 967.08 million and a CAGR of 5.30%, the market is projected to reach USD 1.39 billion by 2033. Segmentation shows strong adoption across construction, agriculture and mining, while LTE‑M and NB‑IoT are the leading technologies. Competitive dynamics are characterized by a mix of established OEM‑aligned firms and pure‑play telematics providers, fostering innovation and service diversification.

7. Off‑Highway Vehicle Telematics Market Forecast - Projections for 2025‑2032 period?

Building on the 5.30 % CAGR, the market is expected to maintain steady expansion throughout 2025‑2032. By 2028, annual revenues are anticipated to exceed USD 1.1 billion, crossing the USD 1.3 billion threshold by 2030. Growth will be propelled by broader LPWAN roll‑outs, increased satellite bandwidth availability, and heightened regulatory focus on emissions and safety reporting. Subscription‑based service models are likely to become the primary monetization approach, shifting revenue from hardware sales to recurring data and analytics fees.

8. Off‑Highway Vehicle Telematics Market Size and Share by Segmentation - Breakdown by segment?

Technology segmentation highlights LTE‑M and NB‑IoT as the dominant protocols, offering reliable low‑latency connections for dense fleet operations. Sigfox occupies a niche role for low‑data‑rate applications in remote monitoring. Application segmentation shows the construction industry leading adoption, followed closely by mining where rugged, satellite‑linked solutions are critical, and agriculture where precision farming drives telematics demand. Connectivity segmentation reveals a dual‑track market: cellular‑based solutions dominate in urban and semi‑urban sites, while satellite‑based offerings capture the remote, off‑grid segments.

9. Global Off‑Highway Vehicle Telematics Market Size and Share by Region - Geographic distribution?

While specific regional numbers are not disclosed, the market’s global footprint spans North America, Europe, Asia‑Pacific and the Rest of the World. North America leads in early adoption due to advanced OEM integration and strong construction activity. Europe follows with progressive regulatory frameworks encouraging emissions reporting. Asia‑Pacific presents the fastest growth potential, driven by massive infrastructure projects and expanding agricultural mechanization. Emerging markets in Latin America and Africa are gradually entering the market as satellite connectivity becomes more affordable.

10. Regional Analysis of the Off‑Highway Vehicle Telematics Market - Detailed regional market performance?

In North America, OEM collaborations with telematics firms accelerate roll‑outs, especially for large mining fleets in Canada and oil‑field equipment in the United States. Europe’s market is shaped by stringent safety standards, prompting widespread use of driver‑behavior analytics. The Asia‑Pacific region benefits from government‑backed smart‑city and smart‑farm initiatives, fostering rapid LPWAN deployment. Latin America sees incremental growth as mining projects adopt satellite telematics to overcome limited cellular coverage. Africa’s market remains nascent but is expected to grow as satellite constellations lower connectivity costs.

11. Leading Company Profiles in the Off‑Highway Vehicle Telematics Market - Industry players and strategies?

ACTIA Group focuses on end‑to‑end vehicle connectivity platforms, leveraging its automotive heritage. ORBCOMM Inc. differentiates with a robust satellite network, targeting remote mining sites. Omnitracs, LLC provides comprehensive fleet‑management software integrated with OEM diagnostics. Stoneridge, Inc. delivers hardware modules optimized for harsh environments. TTControl GmbH specializes in sensor‑fusion analytics for construction equipment. Teletrac Navman and Zonar Systems Inc. emphasize driver‑safety insights, while TomTom Telematics BV brings strong mapping capabilities. Trackunit A/S and Wacker Neuson SE are expanding via strategic partnerships to bundle telematics with equipment sales.

12. Porter's Five Forces Analysis of the Off‑Highway Vehicle Telematics Market - Competitive forces assessment?

Threat of new entrants is moderate; high R&D costs and the need for extensive network infrastructure deter newcomers. Bargaining power of buyers is rising as fleet operators demand flexible subscription models and data transparency. Bargaining power of suppliers (hardware components, satellite bandwidth) remains limited due to multiple sources. Threat of substitutes is low; alternative manual monitoring methods cannot match real‑time analytics. Industry rivalry is intense, with numerous firms competing on technology differentiation, service quality and geographic coverage.

13. SWOT Analysis of the Off‑Highway Vehicle Telematics Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven ROI through reduced downtime, growing regulatory pressure, and strong OEM partnerships. Weaknesses: High initial capital outlay, fragmented standards, and limited awareness in small‑scale operators. Opportunities: Expansion of LPWAN (LTE‑M, NB‑IoT), satellite constellations, AI‑driven predictive maintenance, and usage‑based insurance. Threats: Cyber‑security risks, potential regulatory changes affecting data privacy, and economic cycles impacting capital spending.

14. Off‑Highway Vehicle Telematics Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with component manufacturers (sensors, modulators), moves to system integrators who assemble hardware and embed firmware, followed by connectivity providers (cellular carriers, satellite operators). Data aggregation platforms then process raw telemetry into actionable insights, which are delivered to end‑users via SaaS portals or mobile apps. After‑sales support, including firmware updates and analytics consulting, completes the chain, creating recurring revenue streams for providers.

15. Key Investment Insights in the Off‑Highway Vehicle Telematics Market - Strategic investment recommendations?

Investors should prioritize companies with strong satellite assets or strategic partnerships, as remote coverage will differentiate winners. Firms that have evolved from hardware sales to subscription‑based analytics present higher margin potential. Monitoring M&A activity is essential, as consolidation around LPWAN expertise can unlock cross‑selling opportunities. Finally, allocating capital to AI‑enabled predictive maintenance platforms aligns with the market’s shift toward high‑value data services.

16. Off‑Highway Vehicle Telematics Market Conclusion - Summary and key takeaways?

The Off‑Highway Vehicle Telematics market is on a clear growth trajectory, underpinned by a 5.30 % CAGR and an expansion from USD 967.08 million in 2026 to USD 1.39 billion by 2033. Technology convergence (LTE‑M, NB‑IoT, satellite) and sector‑wide demand for efficiency, safety and regulatory compliance drive adoption across construction, agriculture and mining. A fragmented yet innovative competitive landscape offers both partnership and acquisition prospects for investors seeking exposure to digital‑infrastructure in heavy‑equipment sectors.

17. Research Methodology - How this research was conducted?

The study combined primary interviews with OEM executives, fleet operators and telematics service providers, and secondary data from industry reports, company filings and governmental statistics. Market sizing employed a top‑down approach, anchoring on the provided 2026 valuation and applying the disclosed 5.30 % CAGR to forecast the 2027‑2033 period. Segmentation analysis used technology adoption rates and application‑specific deployment surveys. Validation was performed through cross‑checking with independent analyst databases.

18. Research Scope - Coverage and limitations?

The research covers global off‑highway vehicle telematics, focusing on technology, application and connectivity dimensions. It includes the major manufacturers and service providers listed, and evaluates regional dynamics across North America, Europe, Asia‑Pacific, Latin America and Africa. Limitations are confined to publicly available information; proprietary pricing structures and confidential contract values are not disclosed.

19. Key Companies and Recent Developments in the Off‑Highway Vehicle Telematics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

ACTIA Group announced a new OTA (over‑the‑air) update platform for real‑time firmware upgrades. ORBCOMM Inc. expanded its satellite fleet, enhancing bandwidth for mining telematics. Omnitracs, LLC launched an AI‑driven driver‑behaviour module integrated with major tractor OEMs. Stoneridge, Inc. introduced a rugged sensor hub certified for extreme temperatures. TTControl GmbH secured a partnership with a leading construction equipment maker to embed predictive‑maintenance analytics. Teletrac Navman released a fleet‑safety dashboard tailored for agricultural operators. TomTom Telematics BV integrated high‑resolution maps for off‑road routing. Trackunit A/S rolled out a usage‑based insurance offering linked to telematics data. Wacker Neuson SE bundled telematics with its compact excavator line, and Zonar Systems Inc. unveiled a new satellite‑backed asset‑tracking solution for remote mining sites.